Friday, April 30th

Provided by the SBA

Registration for the SBA application portal is now open. Applications will open on Monday, May 3, 2021, at 11:00AM CST. See the information below (April 23rd) for more details.

For assistance preparing your application, you can access the following:

Friday, April 23rd

Provided by the SBA

SBA to launch Restaurant Revitalization Fund

The American Rescue Plan Act established the Restaurant Revitalization Fund (RRF) to provide funding to help restaurants and other eligible businesses keep their doors open. This program will provide restaurants with funding equal to their pandemic-related revenue loss up to $10 million per business and no more than $5 million per physical location. Recipients are not required to repay the funding as long as funds are used for eligible uses no later than March 11, 2023.

Who can apply

Eligible entities who have experienced pandemic-related revenue loss include:

- Restaurants

- Food stands, food trucks, food carts

- Caterers

- Bars, saloons, lounges, taverns

- Snack and nonalcoholic beverage bars

- Bakeries (onsite sales to the public comprise at least 33% of gross receipts)

- Brewpubs, tasting rooms, taprooms (onsite sales to the public comprise at least 33% of gross receipts)

- Breweries and/or microbreweries (onsite sales to the public comprise at least 33% of gross receipts)

- Wineries and distilleries (onsite sales to the public comprise at least 33% of gross receipts)

- Inns (onsite sales of food and beverage to the public comprise at least 33% of gross receipts)

- Licensed facilities or premises of a beverage alcohol producer where the public may taste, sample, or purchase products

How to apply

You can apply through SBA-recognized Point of Sale (POS) vendors or directly via SBA in a forthcoming online application portal: https://restaurants.sba.gov. Participating POS providers include Square, Toast, Clover, NCR Corporation (Aloha). If you are working with Square or Toast, you do not need to register beforehand on the https://restaurants.sba.gov application portal.

Registration with SAM.gov is not required. DUNS or CAGE identifiers are also not required.

If you would like to prepare your application, view the sample application form. You will be able to complete this form online. Please do not submit RRF forms to SBA at this time.

SBA Form 3172

Additional documentation required:

- Verification for Tax Information: IRS Form 4506-T, completed and signed by Applicant. Completion of this form digitally on the SBA platform will satisfy this requirement.

- Gross Receipts Documentation: Any of the following documents demonstrating gross receipts and, if applicable, eligible expenses ◦Business tax returns (IRS Form 1120 or IRS 1120-S)

- IRS Forms 1040 Schedule C; IRS Forms 1040 Schedule F

- For a partnership: partnership’s IRS Form 1065 (including K-1s)

- Bank statements

- Externally or internally prepared financial statements such as Income Statements or Profit and Loss Statements

- Point of sale report(s), including IRS Form 1099-K

For applicants that are a brewpub, tasting room, taproom, brewery, winery, distillery, or bakery:

- Documents evidencing that onsite sales to the public comprise at least 33.00% of gross receipts for 2019, which may include Tax and Trade Bureau (TTB) Forms 5130.9 or TTB. For businesses who opened in 2020, the Applicant’s original business model should have contemplated at least 33.00% of gross receipts in onsite sales to the public.

For applicants that are an inn:

- Documents evidencing that onsite sales of food and beverage to the public comprise at least 33.00% of gross receipts for 2019. For businesses who opened in 2020, the Applicant’s original business model should have contemplated at least 33.00% of gross receipts in onsite sales to the public.

When to apply

- Priority period: Days 1 through 21

- SBA will accept applications from all eligible applicants, but only process and fund priority group applications.

- A small business concern that is at least 51 percent owned by one or more individuals who are:

- Women, or

- Veterans, or

- Socially and economically disadvantaged (see below).

- Applicants must self-certify on the application that they meet eligibility requirements

- Socially disadvantaged individuals are those who have been subjected to racial or ethnic prejudice or cultural bias because of their identity as a member of a group without regard to their individual qualities.

- Economically disadvantaged individuals are those socially disadvantaged individuals whose ability to compete in the free enterprise system has been impaired due to diminished capital and credit opportunities as compared to others in the same business area who are not socially disadvantaged.

- During this period, SBA will fund applications where the applicant has self-certified that it meets the eligibility requirements for a small business owned by women, veterans, or socially and economically disadvantaged individuals.

- Open to all applicants: Days 22 through funds exhaustion

- SBA will accept applications from all eligible applicants and process applications in the order in which they are approved by SBA

Set asides

- $5 billion is set aside for applicants with 2019 gross receipts of not more than $500,000

- An additional $4 billion is set-aside for applicants with 2019 gross receipts from $500,001 to $1,500,000

- An additional $500 million is set-aside for applicants with 2019 gross receipts of not more than $50,000

*SBA reserves the right to reallocate these funds at the discretion of the Administrator.

Funding amount

Payment calculations:

- Calculation 1: for applicants in operation prior to or on January 1, 2019:

- 2019 gross receipts minus 2020 gross receipts minus PPP loan amounts

- Calculation 2: for applicants that began operations partially through 2019:

- (Average 2019 monthly gross receipts x 12) minus 2020 gross receipts minus PPP loan amounts

- Calculation 3: for applicants that began operations on or between January 1, 2020 and March 10, 2021 and applicants not yet opened but have incurred eligible expenses:

- Amount spent on eligible expenses between February 15, 2020 and March 11, 2021 minus 2020 gross receipts minus 2021 gross receipts (through March 11, 2021) minus PPP loan amounts

- For those entities who began operations partially through 2019, you may elect (at your own discretion) to use either calculation 2 or calculation 3.

Maximum and minimum amounts

SBA may provide funding up to $5 million per location, not to exceed $10 million total for the applicant and any affiliated businesses. The minimum award is $1,000.

Gross receipts

For the purposes of this program, gross receipts does not include:

- Amounts received from Paycheck Protection Program (PPP) loans (First Draw or Second Draw)

- Amounts received from Economic Injury Disaster Loans (EIDL)

- Advances on EIDL (EIDL Advance and Targeted EIDL Advance)

- State and local grants (via CARES Act or otherwise)

- SBA Section 1112 payments

Allowable use of funds

Funds may be used for specific expenses including:

- Business payroll costs (including sick leave)

- Payments on any business mortgage obligation

- Business rent payments (note: this does not include prepayment of rent)

- Business debt service (both principal and interest; note: this does not include any prepayment of principal or interest)

- Business utility payments

- Business maintenance expenses

- Construction of outdoor seating

- Business supplies (including protective equipment and cleaning materials)

- Business food and beverage expenses (including raw materials)

- Covered supplier costs

- Business operating expenses

Get help with your application

For assistance preparing your application, you can access the following:

Supplemental documents

Monday, March 22nd

We're here for you!

As a reminder, we are committed to the health and safety of our customers and employees, so if you're feeling unwell please utilize an alternative to in-person banking until you are well again! The alternatives include:

Interactive Teller Machines (ITMs)

Online and Mobile Banking

Mobile Deposit

Online Account Opening

Phone Calls

Email

Monday, March 15th

Provided by Iowa Bankers Association

Round Three of EIP Disbursements to Start Immediately

On Thursday (March 11th), President Biden signed into law the $1.9 trillion COVID-19 relief bill, the American Rescue Plan Act of 2021. Among other things, the bill authorizes another round of $1,400 per person economic impact payments that will be paid to eligible taxpayers.

The IRS said it expects to send the first batch of about 95 million ACH files today for payment on Wednesday, March 17th. The U.S. Department of the Treasury has collected banking information that will enable them to send EIPs to more than 100 million recipients via the ACH network.

Paper checks will also be part of the rollout. The Bureau of the Fiscal Service will begin printing and mailing checks as soon as they receive recipient information from the IRS. The bureau has the capacity to print and mail one million checks per day. In addition to paper checks, the bureau will also send prepaid cards out to some recipients.

One important note regarding this round of EIPs, the legislation did NOT include a provision protecting the EIPs from garnishments. This means the payments are not considered “protected funds” under the Federal Garnishment rule and banks should apply their normal garnishment procedure to accounts receiving EIPs.

The IRS is working to update its Get My Payment tool, but noted that given the compressed timeframe between the time the bill was signed and the first payment distribution, the tool will only provide status updates for taxpayers who have filed their 2019 or 2020 tax return with direct deposit. The IRS is also working to update its FAQs on the EIPs to provide additional information to taxpayers and payments processors.

Due to the amount of people that may be trying to access their online and mobile banking this week, you may experience slow or failed login attempts. We apologize in advance for any inconvenience. Please sign up for Notifi now, and receive customized account alerts via text or email. You'll be notified as soon as your Economic Impact Payment (EIP) hits your account.

Monday, February 22nd

Provided by Iowa Bankers Association

White House Announces Exclusive Two-Week PPP Application Window or Smallest Firms

The White House today announced several measures to ensure the smallest firms have access to Paycheck Protection Program loans, which includes an exclusive application window for firms with fewer than 20 employees.

Beginning Wednesday and lasting through March 9, only firms with fewer than 20 employees will be eligible to apply for PPP loans. The White House also announced several other measures the U.S. Small Business Administration would implement to help the nation's smallest businesses, including:

- Setting aside $1 billion for PPP loans for sole proprietors, independent contractors and self-employed individuals in low-to-moderate-income areas and revise the loan calculation formula for these applicants. (According to press reports, the revised formula would only be available to new applicants, not retroactive.)

- Eliminating a rule that restricts businesses that are at least 20% owned by an individual who was arrested for or convicted of a felony related to financial assistance fraud in the previous five years or any other felony within the previous year. The restriction will only apply to businesses with applicants or owners who are incarcerated from receiving PPP loans.

- Eliminating a rule restricting businesses at least 20% owned by an individual who is delinquent on student debt from receiving PPP loans.

- Clarifying that noncitizens may apply using individual taxpayer identification numbers.

Thursday, January 14th

Provided by the Small Business Administration (SBA)

First Draw PPP Loans

The Paycheck Protection Program is a loan designed to provide a direct incentive for small businesses to keep their workers on payroll. First Draw PPP Loans can be used to help fund payroll costs, including benefits, and may also be used to pay for mortgage interest, rent, utilities, worker protection costs related to COVID-19, uninsured property damage costs caused by looting or vandalism during 2020, and certain supplier costs and expenses for operations.

SBA will forgive loans if all employee retention criteria are met, and the funds are used for eligible expenses.

- PPP loans have an interest rate of 1%.

- Loans issued prior to June 5, 2020 have a maturity of two years. Loans issued after June 5, 2020 have a maturity of five years.

- Loan payments will be deferred for borrowers who apply for loan forgiveness until SBA remits the borrower's loan forgiveness amount to the lender. If a borrower does not apply for loan forgiveness, payments are deferred 10 months after the end of the covered period for the borrower’s loan forgiveness (either 8 weeks or 24 weeks).

- No collateral or personal guarantees are required.

- Neither the government nor lenders will charge small businesses any fees.

Who may qualify

The following entities affected by Coronavirus (COVID-19) may be eligible:

- Sole proprietors, independent contractors, and self-employed persons

- Any small business concern that meets SBA’s size standards (either the industry size standard or the alternative size standard)

- Any business, 501(c)(3) non-profit organization, 501(c)(19) veterans organization, or tribal business concern (sec. 31(b)(2)(C) of the Small Business Act) with the greater of:

- 500 employees, or

- That meets the SBA industry size standard if more than 500

- Any business with a NAICS code that begins with 72 (Accommodations and Food Services) that has more than one physical location and employs less than 500 per location

How and when to apply

You can apply for a First Draw PPP Loan until March 31, 2021. To promote access for smaller lenders and their customers, SBA will initially only accept Second Draw PPP Loan applications from participating community financial institutions (CFIs). All new First Draw PPP Loans will have the same terms regardless of lender or borrower.

Form 2483- First Draw Borrower Application (updated 1/8/2021)

|

Second Draw PPP Loans

The Paycheck Protection Program (PPP) now allows certain eligible borrowers that previously received a PPP loan to apply for a Second Draw PPP Loan with the same general loan terms as their First Draw PPP Loan.

Second Draw PPP Loans can be used to help fund payroll costs, including benefits. Funds can also be used to pay for mortgage interest, rent, utilities, worker protection costs related to COVID-19, uninsured property damage costs caused by looting or vandalism during 2020, and certain supplier costs and expenses for operations.

Maximum loan amount and increased assistance for accommodation and food services businesses

For most borrowers, the maximum loan amount of a Second Draw PPP Loan is 2.5x average monthly 2019 or 2020 payroll costs up to $2 million. For borrowers in the Accommodation and Food Services sector (use NAICS 72 to confirm), the maximum loan amount for a Second Draw PPP Loan is 3.5x average monthly 2019 or 2020 payroll costs up to $2 million.

Who may qualify

A borrower is generally eligible for a Second Draw PPP Loan if the borrower:

- Previously received a First Draw PPP Loan and will or has used the full amount only for authorized uses

- Has no more than 300 employees; and

- Can demonstrate at least a 25% reduction in gross receipts between comparable quarters in 2019 and 2020

How and when to apply

You can apply for a Second Draw PPP Loan from January 13, 2021, until March 31, 2021. To promote access for smaller lenders and their customers, SBA will initially only accept Second Draw PPP Loan applications from participating community financial institutions (CFIs).

Form 2483-SD- Second Draw Borrower Application (Released 1/8/21)

|

Thursday, January 7th

Provided by ABA

SBA Releases Details, Rules for PPP Relaunch

Community financial institutions will be able to submit loan applications for the Small Business Administration’s Paycheck Protection Program for at least two days before other lenders, SBA said late last night as it released interim final rules covering the pending relaunch of the PPP. However, SBA did not announce the date on which it will reopen its portal for applications for the $284 billion round.

The dedicated window for community financial institutions is part of SBA’s efforts to ensure businesses that most need PPP funds can get them. While noting that “PPP loans have been broadly distributed across diverse areas of the economy, with 27% of the funds going to low- and moderate-income communities, which is in proportion to their percentage of the population,” the law reauthorizing the PPP set aside specific pools of funds for first-time PPP borrowers, very small businesses and small businesses in LMI neighborhoods, as well as for loans from community financial institutions.

The first interim final rule amends the existing PPP rules to reflect changes made by Congress, including on fees, borrower eligibility, loan amounts, eligible expenses, reliance on borrower certifications and loan increases, as well as a new registration requirement for all lenders. However, “most of this document restates existing regulatory provisions to provide lenders and new PPP borrowers a single regulation to consult on borrower eligibility, lender eligibility and loan application and origination requirements, as well as general rules on increases and loan forgiveness for PPP loans,” SBA said.

Meanwhile, the second rule governs the second-draw loans now available for borrowers with 300 or fewer employees, that saw a 25% or greater revenue drop in 2020 compared to 2019 and that have used the full amount of their first-draw PPP loan. “Second-Draw PPP Loans are generally subject to the same terms, conditions and requirements as First-Draw PPP Loans,” SBA said. The maximum loan amount is $2 million or two and a half months’ worth of average payroll costs, whichever is less. The rule covers several calculations to determine eligibility and loan amounts.

Wednesday, January 6th

5 tips to spot Economic Impact Payment (EIP) scams:

- Your bank, or the IRS will not call and ask you to confirm any personal or financial information

- Do not give out your information. If you get a call that is suspicious, it's okay to hang up, look up the number to your bank, the IRS or said agency calling and call them back directly to verify.

- Your bank, or the IRS, will not email you, text you, or contact you on social media to verify your information for EIPs

- Do not open any attachments or click on any links you're not expecting. Delete these messages immediately.

- No one can expedite the payment process

- If someone offers to get you your EIP faster, it's a scam. There is no way to speed up the IRS payment process.

- Look out for bogus checks if your payment is coming through the mail

- Paper checks have been mailed to individuals without direct deposit. If you receive a "check" for an unusual amount, or a "check" that requires verification online or by phone, it's a scam.

- There is no up-front payment, fee or charge of any kind to receive the EIP

- Only scammers will ask you to pay to receive your EIP money.

Tuesday, January 5th

Provided by the IRS

The IRS updated the Get My Payment tool with information related to the second round of Economic Impact Payments. There is currently heavy demand on the tool given the large number of payments going out and people using the tool.

While the IRS has been able to deliver the second round of Economic Impact Payments in record time, we understand there are many questions and we appreciate everyone's patience during this period.

Here are answers to some common questions coming up related to Get My Payment and the second round of Economic Impact Payments.

- I'm having trouble accessing the Get My Payment tool.

- Some people visiting the site may get a "please wait" or error message due to the high volumes coming in. The "please wait" message is a normal part of the site's operation. We encourage people to check back later. Also, there is a limit to the number of times people can access Get My Payment each day. When people reach the maximum number of accesses, Get My Payment will inform them they will need to check back the following day.

- I didn't receive a direct deposit yet. Will I get a second Economic Impact Payment?

- Maybe. IRS updated Get My Payment (GMP) for individuals who are receiving the second Economic Impact Payment on January 5, 2021. If you checked GMP on or after January 5 then:

- If GMP reflects a direct deposit date and partial account information, then your payment is deposited there.

- If GMP reflects a date your payment was mailed, it may take up to 3 – 4 weeks for you to receive the payment. Watch your mail carefully for a check or debit card. (See the FAQ for EIP Card)

- If GMP shows "Payment Status #2 – Not Available," then you will not receive a second Economic Impact Payment and instead you need to claim the Recovery Rebate Credit on your 2020 Tax Return.

- Because of the speed at which the law required the IRS to issue the second round of Economic Impact Payments, some payments may have been sent to an account that may be closed or, is or no longer active, or unfamiliar. By law, the financial institution must return the payment to the IRS; they cannot hold and issue the payment to an individual when the account is no longer active. If Get My Payment shows "Payment Status #2 – Not Available" you will not receive a second EIP.

- The IRS advises people that if they don't receive their Economic Impact Payment, they should file their 2020 tax return electronically and claim the Recovery Rebate Credit on their tax return to get their payment and any refund as quickly as possible.

- What if I have a different bank account than I had on my 2019 tax return? What should I do?

- If the second Economic Impact Payment was sent to an account that is closed or is no longer active the financial institution must , by law, return the payment to the IRS, they cannot hold and issue the payment to an individual when the account is no longer active. The IRS advises people that if they don't receive the full Economic Impact Payment they should file their 2020 tax return electronically and claim the Recovery Rebate Credit on their tax return to get their payment and any refund as quickly as possible.

- Why can't the IRS reissue the second Economic Impact Payment to me?

- The IRS is working hard to deliver the second Economic Impact Payment quickly, as required by law, while still preparing for the upcoming 2021 tax filing season. Due to the compressed timeline, the IRS is unable to reissue and mail checks and instead encourages people to file their 2020 tax return electronically to claim and receive the Recovery Rebate Credit quickly as possible.

- Can I call the IRS, software company or bank to resolve issues with my Economic Impact Payment?

- People should visit IRS.gov for the most current information on the second round of Economic Impact Payments rather than calling the agency or their financial institutions or tax software providers. IRS phone assistors do not have additional information beyond what's available on IRS.gov.

- Where can I get more information?

Monday, January 4th

Online Banking is intermittently unavailable.

Similar to what happened with the last round of Economic Impact Payments (stimulus checks), the vast number of people trying to access their account through online banking is causing your log in attempts to be slow or fail. We apologize for the inconvenience and appreciate your patience as our vendor works to restore service. If you are unable to log in, please call your local branch for account information.

Tuesday, December 29th

Provided by American Bankers Association

On December 21, 2020, Congress authorized, a $900 billion bipartisan coronavirus relief package to provide assistance to American consumers and businesses struggling as a result of the coronavirus pandemic. A provision of the law includes sending government payments to eligible Americans. To help answer common questions about these payments, the American Bankers Association has developed the following questions and answers. We will update the FAQs as we learn more details from the Treasury Department.

How large of a payment will I receive?

The Internal Revenue Service is the agency responsible for determining eligibility. In general, single adults with an adjusted gross income of $75,000 or less will get $600. The $600 limit will also apply to dependents. So, married couples earning a combined adjusted gross income of $150,000 or less with two kids, will receive a total of $2,400. Individual and married taxpayers earning over $75,000 and $150,000 respectively will get reduced payments with full phase-outs at $99,000 and $198,000.

For complete eligibility information please visit the IRS website.

|

When will I receive my payment?

We expect more than 130 million payments to be made via ACH in the first three weeks in January.

If you filed taxes in 2019 and included your bank routing and account number for payments or refunds, and this information has not changed, the IRS has the information it needs to send your payment electronically. In addition, for Social Security recipients, the IRS will use direct deposit by the Social Security Administration to facilitate payments. If the direct deposit information you have provided in the past is for a bank-issued prepaid debit card, you will receive your funds on that card account.

You can check the status of your payment by visiting the IRS' "Get My Payment" web tool. Recipients will be mailed a check if the IRS does not have your information on file. Check payments will follow weeks or possibly months after the direct deposits are sent.

|

What can I do to prevent fraudsters from accessing my funds?

There will be a large amount of funds disbursed to qualifying individuals. Accordingly, there is a risk for fraud of various types. The IRS has announced various ways individuals can be on guard against these types of bad activities. See the notice.

It is important to remember that banks or the federal government will never contact you by telephone, text or email asking for your account information. Do not provide any banking information to anyone claiming to be registering you for your relief payment.

|

What happens if a payment is made to someone who is deceased?

The legislation states that eligible recipients that were alive as of 1/1/20 are enabled to receive EIPs. If the recipients dies between 1/1/20 and receiving the EIP, that payment remains valid. These payments would be accepted through the deceased's estate.

|

Due to social distancing and upcoming economic impact payments, wait times in branches may increase. We strongly encourage you to use the free Frontier Bank mobile app and mobile deposit, or an ITM as a first choice for making deposits. You may also set up Notifi through your online banking to alert you via text or email when deposits or other specified activity happens within your account.

Monday, December 28th

Provided by American Bankers Association

COVID-19 EIP Transactions Expected to Land As Soon as Tomorrow

After President Trump signed the COVID-19 economic relief bill Sunday night, bankers should expect to see ACH transactions for the $600-per-person economic impact payments (EIP) begin arriving as soon as tomorrow, Dec. 29. More than 100 million files are expected to be routed to banks in the coming days with an effective payment date early next week, according to sources. Checks and prepaid cards will be mailed to recipients that have not provided their bank routing information to the Internal Revenue Service. The Treasury Department is expected to release more detailed information soon.

EIP Benefits

The maximum payment for an individual is $600. The $600 limit will also apply to dependents. This means that a family of four could receive a payment of $2,400. The maximum benefits will apply to individuals with an income below $75,000 per their 2019 tax returns. Those with incomes higher than $75,000 will receive a prorated amount until the cut-off income of $87,000, if they have no dependents. For couples, the full benefit will apply to those earning up to $150,000 and will taper off as their income approaches $174,000.

EIP Timing

The U.S. Department of the Treasury has collected banking information that will enable them to send EIPs to approximately 130 million recipients via the ACH network. There are indications that these payments will be made in just a few days to get the funds into recipient accounts quickly. It is possible that more than 110 million EIPs ACH transactions could be sent on one day. Batches of EIPs could be arriving this week.

Paper checks will also be part of the rollout. The Bureau of the Fiscal Service (BFS) will begin printing and mailing checks as soon as they receive recipient information from the Internal Revenue Service (IRS). The BFS has the capacity to print and mail one million checks per day.

In addition to paper checks, BFS will also be sending prepaid cards out to some of the recipients that aren’t enabled to receive ACH payments.

Tuesday, December 22nd

Provided by the Iowa Bankers Association

Congress Expected to Pass COVID Relief Soon

After weeks of negotiations, congressional leaders announced a deal Sunday for a $900 billion bipartisan coronavirus relief package, and Congress is expected to vote on the legislation tonight.

The deal reportedly includes more than $284 billion in new funds for the Paycheck Protection Program. That includes a second draw option for prior PPP borrowers who have less than 300 employees and can demonstrate a 25% decline in gross receipts in one quarter of 2020 relative to that same quarter in 2019. The relief package also expands eligibility for PPP loans and simplifies the forgiveness process for loans under $150,000.

A new round of economic impact payments is also included in the legislation. A payment of up to $600 per person, including children, for families earning up to $150,000 a year. U.S. Treasury Secretary Steven Mnuchin said recipients of EIPs would start seeing the money in their bank accounts early next week.

Read a summary of the bill's provisions for economic aid for small businesses.

Monday, December 14th

As you may have seen by the South Dakota's governor’s press release Friday, there will be a second round of grant applications for businesses affected by COVID-19 that will open up today, around noon CST and will remain open until December 20, 2020.

The new grant opportunity will be for the time period of September – November. The grant criteria from the first round will stay the same for small businesses and non-profit businesses. Start-up businesses who applied during the first round will also be eligible.

For returning applicants, the required information will be very condensed. You will need to fill out a new application, using the same log-in on the same application portal (https://sdcovidhelp.force.com/Grants/s/login/). In addition, you’ll need to upload the following documentation:

- P & L Statement for 9/1 – 11/30 for both 2019 and 2020, or other supporting documentation (bank statements, expense register, etc. – these items are only required if the applicant is submitting handwritten documents) The numbers input into the application must match the numbers on the P&L/supporting documentation, so I would recommend adding a note if there are adjustments that are made to the numbers. There is a new box in the application for this to make it easier. This will all make the review process go a lot smoother, and more importantly – quicker.

- If a business’s annual revenue was less than $150,000 in 2019, they do not need to submit a P&L or other supporting documentation. The information input into the application will be used instead, just like during the first round.

For new applicants, here is the information you should have handy and ready to submit:

- Certificate of Good Standing from the Secretary of State’s Office (a screenshot showing proof of good standing is acceptable. See attached for an example.) For sole proprietors, they should submit a copy of their tax license from the Department of Revenue. If the business does not have either, they should attach a document of explanation of why they don’t have either.

- Government-issued ID of authorized business owner

- W-9

- 2019 Tax return

- P & L Statement for 9/1 – 11/30 for both 2019 and 2020, or other supporting documentation (bank statements, expense register, etc. – these items are only required if the applicant is submitting handwritten documents) The numbers input into the application must match the numbers on the P&L/supporting documentation, so I would recommend adding a note if there are adjustments that are made to the numbers. There is a new box in the application for this to make it easier. This will all make the review process go a lot smoother, and more importantly – quicker.

- Information regarding all COVID aid for 2020. Like the first round, any federal grant amount, like PPP, will need to be deducted from the potential grant award. For businesses who may have had PPP loans or other aid, they will be given the voluntary opportunity to provide their March – August financial numbers and statements so that the aid could be counted against any potential losses during that time period. It’s important to note that they would not be eligible to receive any funding for the March – August loss if they did not apply during the first round, but providing the numbers & documentation has the potential to help for this round of funding.

For more information, please visit https://covid.sd.gov/smallbusiness-healthcare-grants.aspx.

Tuesday, October 13th

SBA and Treasury have announced the issuance of SBA Form 3508S- which is a simpler forgiveness application process for loans of $50,000 or less.

WASHINGTON—The U.S. Small Business Administration, in consultation with the Treasury Department, today (Thursday, October 8th) released a simpler loan forgiveness application for Paycheck Protection Program (PPP) loans of $50,000 or less. This action streamlines the PPP forgiveness process to provide financial and administrative relief to America’s smallest businesses while also ensuring sound stewardship of taxpayer dollars.

“The PPP has provided 5.2 million loans worth $525 billion to American small businesses, providing critical economic relief and supporting more than 51 million jobs,” said Secretary Steven T. Mnuchin. “Today’s action streamlines the forgiveness process for PPP borrowers with loans of $50,000 or less and thousands of PPP lenders who worked around the clock to process loans quickly,” he continued. “We are committed to making the PPP forgiveness process as simple as possible while also protecting against fraud and misuse of funds. We continue to favor additional legislation to further simplify the forgiveness process.”

“Nothing will stop the Trump Administration from supporting great American businesses and our great American workers. The Paycheck Protection Program has been an overwhelming success and served as a historic lifeline to America’s hurting small businesses and tens of millions of workers. The new form introduced today demonstrates our relentless commitment to using every tool in our toolbelt to help small businesses and the banks that have participated in this program,” said Administrator Jovita Carranza. “We are continuing to ensure that small businesses are supported as they recover.”

SBA and Treasury have also eased the burden on PPP lenders, allowing lenders to process forgiveness applications more swiftly.

SBA began approving PPP forgiveness applications and remitting forgiveness payments to PPP lenders for PPP borrowers on October 2, 2020. SBA will continue to process all PPP forgiveness applications in an expeditious manner.

Documents provided by the SBA:

Tuesday, October 13th

The State of South Dakota received $1,250,000,000 in federal funds to be used for costs incurred due to the public health emergency in response to the Coronavirus Disease 2019 (COVID-19). In consultation with the legislature, the Administration has determined that the unexpended portion of these coronavirus relief funds to be spent on several different programs aimed at supporting small businesses and healthcare providers across the State.

Any legal business, including farms and ranches are eligible- but they all will be required to disclose federal COVID grant funding received this year, including CFAP (Coronavirus Food Assistance Program and PPP.)

For more information visit, https://covid.sd.gov/smallbusiness-healthcare-grants.aspx.

Contact covid.bizgrants@state.sd.us or 605-937-7243 with questions. The call enter is open Monday-Friday, 8:00am-5:00pm.

Thursday, September 10th

Governor Noem Outlines Framework for $400 Million in CARES Act Funding for South Dakota Small Businesses

PIERRE, S.D. - Today, Governor Kristi Noem laid out a framework for up to $400 million in Coronavirus Relief Funds (CRF) to assist South Dakota’s small businesses negatively impacted by the COVID-19 pandemic.

“South Dakota is in a good spot as we rebound from COVID-19, but some of our small businesses were still hurt by this pandemic,” said Governor Noem. “These folks are the lifeblood of our communities and economy. When I asked folks to adjust their way of life to help us flatten the curve, South Dakotans exercised their personal responsibility and responded. That adjustment significantly impacted the day-to-day operations, customer traffic, and supply chains of a number of small business owners across our state. It’s my hope that this proposal will help folks stay open and overcome the unprecedented times we’ve faced these last several months. I’m looking forward to discussing it with the legislature.”

Under Governor Noem’s proposal, businesses would qualify for this grant if they are located in South Dakota, have at least $50,000 in gross revenue in 2019, and have had a reduction in business of at least 25% between March and May as a result of COVID-19. The calculation for “reduction in business” can be found here.

The proposed application period for the program would open on October 12 and close on October 23. Grants would be rewarded once all applications are received. Following the initial reward period, a second allocation of funds would be considered if additional funds are still available. Under current federal law, all funds must be distributed by December 30, 2020. Grants would be awarded up to $100,000 per qualifying business.

To learn more about this framework and the fight against the COVID-19 pandemic in South Dakota, please visit COVID.sd.gov.

Tuesday, September 1st

Applications Open for Two State Ag Grants- The State of Iowa began accepting applications today for two agricultural grants funded with money provided by the CARES Act.

Wednesday, August 12th

We are now accepting Paycheck Protection Program (PPP) loan forgiveness applications!

As part of the PPP Flexibility Act, the SBA and Treasury released two versions of loan forgiveness applications: a revised PPP Loan Forgiveness Application and an EZ PPP Loan Forgiveness Application. You can find both applications and their respective instruction sheets below. Please review the two applications and required documentation (found on each application’s instruction sheet) to determine which application may pertain to your business. Please contact your local Frontier Bank lender with questions or for assistance.

You may be able to use the simplified EZ version of the application if you can certify any of the following three items:

- You are self-employed and have no employees; OR

- You did not reduce the salaries or wages of your employees by more than 25% and did not reduce the number or hours of your employees; OR

- You experienced reductions in business activity as a result of health directives related to COVID-19 and did not reduce the salaries or wages of your employees by more than 25%

Monday, July 20th

Provided by Iowa Economic Development Authority

ASSISTANCE FOR IOWA SMALL BUSINESSES & NONPROFITS

Governor Reynolds has allocated federal CARES Act funds to assist small businesses and nonprofits who have been economically impacted by COVID-19. The Iowa Economic Development Authority’s Small Business Utility Disruption Prevention Program will provide short-term relief to eligible small businesses and nonprofits that face significant hardship in the payment of utility bills for service provided during the months of disruption to their business.

AVAILABLE UTILITY BILL ASSISTANCE

- Electric and natural gas utility bill assistance for actual utility debt incurred for electric or natural gas service provided between March 17, 2020 and June 30, 2020, not to exceed $7,500.

- Financial assistance can only be applied to the applicants’ utility bills. The applicants’ utility service provider will receive a credit, which will be applied to the applicants’ utility debt.

- Applications will be accepted on an ongoing basis beginning July 17, 2020, and assistance will be provided to eligible applicants on a first come, first ready to proceed basis until all funds have been exhausted or August 21, 2020, whichever comes first.

ELIGIBILITY

- Iowa-based for profit and nonprofit businesses with 50 or fewer employees

- Must have a physical location (non-residential) in Iowa

- Must be registered with the Iowa Secretary of State to do business in the State of Iowa

- Must not be an ineligible business type:

- Adult Entertainment; Construction, Internet Sales, without corresponding storefront; Medical; Private Clubs, Professional Services; Professional Sports; Religious Institutions, with the exception of those offering social services including daycare, food bank, preschool, shelter, etc.

- Have not received funds provided by the State of Iowa's Small Business Relief Grant (SBRG) funding

- Have not received any funds provided by the State of Iowa's Nonprofit Recovery Fund

- Must have experienced a COVID-19 loss of revenue on or after March 17, 2020 that resulted in unpaid bills for electric or natural gas utility service provided between March 17, 2020 and June 30, 2020

- Applicants' average monthly electric usage must not exceed 25,000 kWh for electricity or 2,500 therms for natural gas (review with your utility bill and/or contact your utility provider to confirm)

- Businesses must be open

REQUIRED DOCUMENTATION

Applicant to complete a payroll template [.XLS] with employee information as of March 1, 2020

HOW TO APPLY

Applicants are required to complete the pre-application screening below. Upon successful completion of this screening checklist, the applicant will be provided with the link to the full application. By clicking below, you confirm you have read the eligibility guidelines and FAQ documentation.

Pre-Application Checklist

Monday, July 6th

Provided by Small Business Administration (SBA)

Notice: Paycheck Protection Program has reopened. The Paycheck Protection Program resumed accepting applications July 6, 2020, at 8:00 AM CST in response to President signing the program's extension legislation. The new deadline to apply for a Paycheck Protection Program loan is August 8, 2020.

Wednesday, June 24th

We have updated our PPP loan forgiveness checklist to reflect the most recent changes. One of the changes includes an update to forgiveness of owner compensation for individuals with self-employment income-

- Forgiveness of owner compensation for individuals with self-employment income filing a Schedule C or F is limited to either 8 weeks’ worth of 2019 net profit (up to $15,385) for an 8-week Covered Period or 2.5 months’ worth of 2019 net profit (up to $20,833) for a 24-week Covered Period

Revised Checklist

Tuesday, June 23rd

Provided by Iowa Bankers Association

The U.S. Small Business Administration issued a new interim final rule Monday implementing regulation changes made to the Paycheck Protection Program loan forgiveness process by the PPP Flexibility Act and other recent developments, including the SBA’s simplified Form 3508EZ forgiveness application. The rule conforms previous rules to reflect provisions of the PPPFA, including the covered period for forgiveness, non-payroll costs eligible for forgiveness, reductions in the forgiven amount and the timing of when borrowers must apply for forgiveness to avoid making payments. It confirms that borrowers may submit forgiveness applications any time on or before the loan matures, including before the end of the covered period, provided they have used all of the loan funds for which they wish to apply for forgiveness. The rule also incorporates exemptions in the PPP Flexibility Act that preserve loan forgiveness for employers that made good-faith attempts to rehire employees or fill vacant positions (and retained a previous exemption for employers that have reduced employee hours and offered in good faith to restore them) or whose business could not return to normal because of public health directives. The SBA interpreted the latter exemption to include “both direct and indirect compliance” with state and local shutdown orders as well as federal guidance. Read the full interim rule.

Thursday, June 18th

Provided by Iowa Bankers Association

SBA streamlines PPP forgiveness application for many PPP borrowers (June 17, 2020): The U.S. Small Business Administration today released a three-page “EZ” Paycheck Protection Program loan forgiveness application requiring less documentation and fewer calculations than previously required. Form 3508EZ applies to borrowers who meet any of these three criteria:

- Applied for the PPP loan as self-employed, an independent contractor or a sole proprietor with no employees.

- Did not reduce salary or wages for any employee by more than 25%, and did not reduce the number or hours of their employees (excepting laid-off employees who refused an offer to return).

- Did not reduce salary or wages for any employee by more than 25% during the covered period and experienced reductions in business activity as a result of health directives related to COVID-19.

The streamlined forgiveness form is expected to smooth the forgiveness application process for a substantial portion of PPP borrowers. The SBA also updated the regular Form 3508 to reflect recent changes made by Congress in the PPP Flexibility Act and issued a new interim final rule that implements changes made by the PPPFA.

Documents provided by the SBA:

Form 3508EZ

Instructions for Form 3508EZ

INSTRUCTION SUMMARY FOR FORM 3508EZ

Revised 3508

Instructions for Form 3508

INSTRUCTION SUMMARY FOR REVISED FORM 3508

REVISED CHECKLIST

Please contact your local lender with questions, or for more information.

Tuesday, June 16th

Provided by the Small Business Association (SBA)

To further meet the needs of U.S. small businesses and non-profits, the U.S. Small Business Administration reopened the Economic Injury Disaster Loan (EIDL) and EIDL Advance program portal to all eligible applicants experiencing economic impacts due to COVID-19 today.

“The SBA is strongly committed to working around the clock, providing dedicated emergency assistance to the small businesses and non-profits that are facing economic disruption due to the COVID-19 impact. With the reopening of the EIDL assistance and EIDL Advance application portal to all new applicants, additional small businesses and non-profits will be able to receive these long-term, low interest loans and emergency grants – reducing the economic impacts for their businesses, employees and communities they support,” said SBA Administrator Jovita Carranza. “Since EIDL assistance due to the pandemic first became available to small businesses located in every state and territory, SBA has worked to provide the greatest amount of emergency economic relief possible. To meet the unprecedented need, the SBA has made numerous improvements to the application and loan closing process, including deploying new technology and automated tools.”

SBA’s EIDL program offers long-term, low interest assistance for a small business or non-profit. These loans can provide vital economic support to help alleviate temporary loss of revenue. EIDL assistance can be used to cover payroll and inventory, pay debt or fund other expenses. Additionally, the EIDL Advance will provide up to $10,000 ($1,000 per employee) of emergency economic relief to businesses that are currently experiencing temporary difficulties, and these emergency grants do not have to be repaid.

SBA’s COVID-19 Economic Injury Disaster Loan (EIDL) and EIDL Advance

- The SBA is offering low interest federal disaster loans for working capital to small businesses and non-profit organizations that are suffering substantial economic injury as a result of COVID-19 in all U.S. states, Washington D.C., and territories.

- These loans may be used to pay debts, payroll, accounts payable and other bills that can’t be paid because of the disaster’s impact, and that are not already covered by a Paycheck Protection Program loan. The interest rate is 3.75% for small businesses. The interest rate for non-profits is 2.75%.

- To keep payments affordable for small businesses, SBA offers loans with long repayment terms, up to a maximum of 30 years. Plus, the first payment is deferred for one year.

In addition, small businesses and non-profits may request, as part of their loan application, an EIDL Advance of up to $10,000.

- The EIDL Advance is designed to provide emergency economic relief to businesses that are currently experiencing a temporary loss of revenue. This advance will not have to be repaid, and small businesses may receive an advance even if they are not approved for a loan.

- SBA’s EIDL and EIDL Advance are just one piece of the expanded focus of the federal government’s coordinated response.

- The SBA is also assisting small businesses and non-profits with access to the federal forgivable loan program, the Paycheck Protection Program (PPP), which is currently accepting applications until June 30, 2020.

Tuesday, June 9th

Provided by Iowa Bankers Association

With the president signing the Paycheck Protection Program Flexibility Act last week, U.S. Treasury Secretary Steven Mnuchin and Jovita Carranza, U.S. Small Business Administration administrator, issued a joint statement promising to issue rules and guidance, a modified borrower application, and a modified loan forgiveness application implementing the changes to the PPP. The bill implements the following changes:

- Extends the covered period for loan forgiveness from eight weeks after the date of loan disbursement to 24 weeks after the date of loan disbursement, providing substantially greater flexibility for borrowers to qualify for loan forgiveness.

- Lowers the requirements that 75% of a borrower’s loan proceeds must be used for payroll costs and that 75% of the loan forgiveness amount must have been spent on payroll costs during the 24-week loan forgiveness covered period to 60% for each of these requirements.

- Provides a safe harbor from reductions in loan forgiveness based on reductions in full-time equivalent employees for borrowers that are unable to return to the same level of business activity the business was operating at before Feb. 15th, due to compliance with requirements or guidance related to worker or customer safety requirements related to COVID–19.

- Provides a safe harbor from reductions in loan forgiveness based on reductions in full-time equivalent employees, to provide protections for borrowers that are both unable to rehire individuals who were employees of the borrower on Feb. 15, and unable to hire similarly qualified employees for unfilled positions by Dec. 31st.

- Increase to five years the maturity of PPP loans that are approved by the SBA on or after June 5th.

- Extends the deferral period for borrower payments of principal, interest and fees on PPP loans to the date that the SBA remits the borrower’s loan forgiveness amount to the lender (or, if the borrower does not apply for loan forgiveness, 10 months after the end of the borrower’s loan forgiveness covered period).

- Confirms that June 30th remains the last date on which a PPP loan application can be approved.

Please disregard the previously posted PPP loan forgiveness application. As stated, they will be issuing a new forgiveness application. We have updated our checklist to accommodate the changes and that is found below. We'll continue to update you with the new information and resources, as soon as we receive them.

Checklist for Forgiveness

Monday, June 8th

Provided by Iowa Bankers Association

President Donald Trump signed the Paycheck Protection Program Flexibility Act Friday. This legislation offers more flexibility for the Paycheck Protection Program to provide aid to small businesses adversely impacted by the coronavirus. The bill extends the window for businesses to spend PPP loans, which was established by $2.2 trillion coronavirus relief legislation signed at the end of March. The bill passed the Senate by unanimous consent on Wednesday after the House approved the bill in a 417-1 vote last week.

Benefits include:

- The original coronavirus relief package gave businesses 8 weeks to spend PPP funds. The bill signed into law Friday extends that period to 24 weeks.

- The 75-25 ratio included in the March bill requiring businesses to spend 75% of the PPP loan on payroll and 25% on other fixed costs, has been adjusted to a 60-40 ratio.

Wednesday, June 3rd

Provided by Iowa Bankers Association

Treasury Department resolves issues with EIP prepaid debit cards (June 2, 2020): The U.S. Treasury Department has resolved several problems with the Economic Impact Payment prepaid debit cards it used to distribute coronavirus stimulus payments. The debit cards have been sent to about 4 million Americans in the past few weeks and nearly all of the cards have been mailed out. Many people threw the cards away, believing they were a credit-card solicitation or a scam. To replace a lost or stolen card, consumers should call 800-240-8100 and press “2” when prompted for a lost or stolen card, and enter the last six digits of their Social Security number. The Treasury Department also said it has increased the daily limit for cash withdrawals from $1,000 to $2,500; allowed recipients to transfer all of the money from their EIP card to a bank account for free; and verified that cards issued with an incorrect last name (such as a spouse’s name) are still valid.

Please contact a customer service representative with questions.

Thursday, May 28th

The Small Business Administration (SBA) has released the Loan Forgiveness Application for the Paycheck Protection Program (PPP) loans.

With some parts of the application being self-explanatory, and other parts being very complex, the SBA promises they will issue further guidance to assist borrowers as they continue to go through applications.

As we wait for the promised guidance, we strongly encourage you to:

- Familiarize yourself with the application

- Document your expenses from your business checking account

- Begin collecting current and prior payroll information

- Keep track of your progress by utilizing the Checklist we've created for you

Things continue to change, and we will continue to notify you of these changes and new information released about the PPP loans as we receive it. We are also frequently updating this blog with new information, so please check here for the most up-to-date information.

Previously posted guidance:

Access the Paycheck Protection Program Loan Forgiveness Instructions and Application

Application Instructions Summary

Tuesday, May 26th

Provided by the Small Business Administration (SBA)

SBA and Treasury released two new Interim Final Rules Friday (May 22nd) night.

The Interim Final Rule on Loan Forgiveness can be found here. It provides some additional details on the loan forgiveness process, but one item we want to highlight is the decision to now allow bonuses and hazard pay as part of forgivable payroll.

- Are salary, wages, or commission payments to furloughed employees; bonuses; or hazard pay during the covered period eligible for loan forgiveness? (From page 11 of the Interim Final Rule on Loan Forgiveness)

- Yes. The CARES Act defines the term “payroll costs” broadly to include compensation in the form of salary, wages, commissions, or similar compensation. If a borrower pays furloughed employees their salary, wages, or commissions during the covered period, those payments are eligible for forgiveness as long as they do not exceed an annual salary of $100,000, as prorated for the covered period. The Administrator, in consultation with the Secretary, has determined that this interpretation is consistent with the text of the statute and advances the paycheck protection purposes of the statute by enabling borrowers to continue paying their employees even if those employees are not able to perform their day-to-day duties, whether due to lack of economic demand or public health considerations. This intent is reflected throughout the statute, including in section 1106(d)(4) of the Act, which provides that additional wages paid to tipped employees are eligible for forgiveness. The Administrator, in consultation with the Secretary, has also determined that, if an employee’s total compensation does not exceed $100,000 on an annualized basis, the employee’s hazard pay and bonuses are eligible for loan forgiveness because they constitute a supplement to salary or wages, and are thus a similar form of compensation.

Tuesday, May 26th

Beginning Monday, June 1st, all Frontier Bank lobbies will be reopening! We're excited to welcome you back, while keeping the health and safety of you and our employee's high priority. We're taking the following precautions to keep everyone safe:

- Wellness advisory signs are posted at our entrances, encouraging those who do not feel well or have recently traveled to a high-risk area to visit at a later date, or use an alternative to in-person banking (ITM, Mobile Deposit, night drop, call or email).

- Plexiglass dividers have been added to our teller stations, conference rooms and a few of our bankers' desks

- Lobbies will be limited to 3 customers at one time, and bankers' desks will be limited to 2 customers at one time

- Floor decals have been placed in our lobbies to encourage social distancing

- We've implemented enhanced cleaning and sanitation measures including:

- sanitizing stations have been added to bank entrances for customer use

- employees will be cleaning teller stations and desks between each customer

- We are highly encouraging masks when social distancing cannot be met; however, we are not requiring customers or employees to wear them

We truly appreciate your understanding and cooperation during this unprecedented time. If you have questions about our safety efforts or the reopening of our locations, please contact us.

Wednesday, May 20th

Provided by the Iowa Bankers Association

Only $100 billion left in Paycheck Protection Program (PPP) funding (May 19, 2020): As of Saturday, the U.S. Small Business Administration has approved more than 2.7 million Paycheck Protection Program loans totaling more than $195 billion during the second round of funding. The IBA was informed Monday that there is $100 billion left in funds. The average loan size during the second round of the program was $70,622. Lenders with more than $50 billion in assets accounted for more than $102.5 billion in loans. Lenders with less than $10 billion in assets accounted for nearly 63 billion in loans. Lenders with assets between $10 billion and $50 billion accounted for nearly $30 billion in loans. Through both rounds, the SBA has guaranteed more than 4.3 billion loans amounting to more than $513 billion. Iowa financial institutions have had 53,419 PPP loans approved, totaling $5.04 billion over the course of the program.

Documents previously provided by the SBA:

PPP APPLICATION

PPP Overview

PPP Information for Borrowers

Please contact your local lender with questions, or to submit an application.

Tuesday, May 19th

Provided by the Small Business Administration (SBA)

Paycheck Protection Program Loan Forgiveness

Forgiveness is based on the employer maintaining or quickly rehiring employees and maintaining salary levels. Forgiveness will be reduced if full-time headcount declines, or if salaries and wages decrease. The loan forgiveness form and instructions include several measures to reduce compliance burdens and simplify the process for borrowers, including:

- Options for borrowers to calculate payroll costs using an “alternative payroll covered period” that aligns with borrowers’ regular payroll cycles

- Flexibility to include eligible payroll and non-payroll expenses paid or incurred during the eight-week period after receiving their PPP loan

- Step-by-step instructions on how to perform the calculations required by the CARES Act to confirm eligibility for loan forgiveness

- Borrower-friendly implementation of statutory exemptions from loan forgiveness reduction based on rehiring by June 30

- Addition of a new exemption from the loan forgiveness reduction for borrowers who have made a good-faith, written offer to rehire workers that was declined

Access the Paycheck Protection Program Loan Forgiveness Instructions and Application

Application Instructions Summary

Wednesday, May 13th

PPP Loan Forgiveness- What we know today

- What costs are eligible for loan forgiveness

- Payroll costs (salaries and wages, subject to $100k cap per employee, employer provided fringe benefits such as vacation, health and retirement benefits, and state unemployment tax payments)

- Interest payments on a mortgage incurred in the ordinary course of business on real or personal property and that was in existence on Feb. 15, 2020

- Rent payments under leasing agreements in existence on Feb. 15, 2020

- Utility payments for which service was in existence on Feb. 15, 2020. SBA guidance did include fuel in a business vehicle as a qualified cost.

- The actual amount of loan forgiveness is based on costs incurred and payments made during the covered 8-week period. Qualifying costs may include:

- Are there limitations on loan forgiveness?

- Not more than 25 percent of the loan forgiveness amount can be attributable to non-payroll costs (i.e., mortgage interest, rent and utilities)

- Proceeds from any advance up to $10,000 on an Economic Injury Disaster Loan (EIDL) will be deducted from the loan forgiveness amount

- A reduction in the number of full-time equivalent employees

- A reduction of individual employee wages by more than 25%

- Yes, loan forgiveness is limited in the following circumstances:

- What terms apply to any loan amount that is not forgiven?

- 2 year term

- 1% interest rate

- No payments required during the first six months

- No prepayment penalty

- The principal amount of the PPP loan will continue on its original terms, including:

- What documentation must be submitted with an application for loan forgiveness?

- Documentation verifying the number of FTE employees and individual wages to prove forgiveness is not limited due to these factors

- Payroll reports and other tax filings, such as W-3 or Form 941

- Tax Return Documents, such as Sch C, F, if applying as a self-employed person or Form 1065, Form 1120 or 1120S for partnerships and corporations

- Documentation, including invoices and cancelled checks for the non-payroll qualifying costs (mortgage interest, rent expense, utilities expense)

- A certification that the information provided is true and correct

- We're still waiting for clear guidance from SBA on loan forgiveness. At a minimum, we expect you will be required to submit:

Because guidance is not currently clear, we strongly encourage detailed record-keeping during your covered 8-week period. It is always a good idea to save all invoices related to your business, but extremely important at this time. Also be sure to make qualifying cost payments out of business checking accounts, where applicable.

If you have questions, please contact your local lender.

Tuesday, May 12th

Looking for a safer way to pay for your essentials during Covid-19? Use a digital wallet! A digital wallet is a phone app or service that can be used to pay for purchases at participating stores. It’s a great a way to make purchases without touching frequently used credit card terminals.

When you link your Frontier Bank debit card to a mobile wallet, your card information is safe, and so are you. Visit our online solutions page to learn more about using your debit or credit card in a digital wallet, or select one of the services below to learn how to link your card.

Apple Pay

Google Pay

Monday, May 4th

Provided by the Small Business Association (SBA)

In response to the Coronavirus (COVID-19) pandemic, small business owners in all U.S. states, Washington D.C., and territories were able to apply for an Economic Injury Disaster Loan advance of up to $10,000. This advance is designed to provide economic relief to businesses that are currently experiencing a temporary loss of revenue. This loan advance will not have to be repaid.

SBA has resumed processing EIDL applications that were submitted before the portal stopped accepting new applications on April 15 and will be processing these applications on a first-come, first-served basis. SBA will begin accepting new Economic Injury Disaster Loan (EIDL) and EIDL Advance applications on a limited basis only to provide relief to U.S. agricultural businesses.

The new eligibility is made possible as a result of the latest round of funds appropriated by Congress in response to the COVID-19 pandemic.

Agricultural businesses includes those businesses engaged in the production of food and fiber, ranching, and raising of livestock, aquaculture, and all other farming and agricultural related industries (as defined by section 18(b) of the Small Business Act (15 U.S.C. 647(b)).

SBA is encouraging all eligible agricultural businesses with 500 or fewer employees wishing to apply to begin preparing their business financial information needed for their application.

At this time, only agricultural business applications will be accepted due to limitations in funding availability and the unprecedented submission of applications already received. Applicants who have already submitted their applications will continue to be processed on a first-come, first-served basis. For agricultural businesses that submitted an EIDL application through the streamlined application portal prior to the legislative change, SBA will process these applications without the need for re-applying.

Eligible agricultural businesses may apply for the Loan Advance here.

Friday, April 24th

Provided by the Small Business Association (SBA)

Administrator of the U.S. Small Business Administration Jovita Carranza and U.S. Treasury Secretary Steven T. Mnuchin issued the following statement today on the resumption of the Payroll Protection Program (PPP):

“We are pleased that President Trump has signed into law the Paycheck Protection Program and Health Care Enhancement Act, which provides critical additional funding for American workers and small businesses affected by the coronavirus pandemic. We want to thank Leader McConnell, Leader Schumer, Speaker Pelosi, and Leader McCarthy for working with us on a bipartisan basis to ensure that the Paycheck Protection Program is funded so that small businesses can keep hardworking Americans on the payroll.

“The Small Business Administration will resume accepting PPP loan applications on Monday, April 27 at 9:30AM CST from approved lenders on behalf of any eligible borrower. This will ensure that SBA has properly coded the system to account for changes made by the legislation.

“The PPP has supported more than 1.66 million small businesses and protected over 30 million jobs for hardworking Americans. With the additional funds appropriated by Congress, tens of millions of additional workers will benefit from this critical relief.

Documents previously provided by the SBA:

PPP APPLICATION

PPP Overview

PPP Information for Borrowers

For questions or to submit an application, contact your local Frontier Bank lender.

Tuesday, April 21st

We're staying one step ahead of the game for if and when Congress releases more funds to help the businesses in our communities get back on the path to success. If you have yet to apply for a SBA Paycheck Protection Plan loan for your business, we are encouraging everyone to do so now. The second new funds are available, we will begin to process your applications.

Documents provided by the SBA:

PPP APPLICATION

PPP Overview

PPP Information for Borrowers

Contact your local Frontier Bank lender to get started.

Friday, April 17th

Provided by Iowa Bankers Association

Economic Impact Payments

- "Get My Payment" Tool is live

- Check your payment status

- If your check is not issued, you can provide account information to receive an ACH instead

- ACH payments have started

- 80 million ACH payments processed this week

- ACH files will be sent out each Friday (volume will vary but probably won't be as large) through the month of May

- Checks

- Checks will be mailed out starting early next week

- 5-7 million checks anticipated each week (volume will vary)

Monday, April 13th

Provided by American Bankers Association (ABA)

Economic Impact Payment FAQ for Consumers

In March, Congress passed—and President Trump signed into law—the CARES Act, a $2 trillion economic relief package to provide assistance to American consumers and businesses struggling as a result of the coronavirus pandemic. A provision of the law includes sending government payments to eligible Americans. To help answer common questions about these payments, the American Bankers Association has developed the following questions and answers.

- How large a payment will I receive?

The CARES Act outlines the parameters of who is eligible to receive a payment. The Internal Revenue Service is the agency responsible for determining eligibility. In general, single adults with an adjusted gross income of $75,000 or less will get $1,200. Married couples earning a combined adjusted gross income of $150,000 or less will receive a total of $2,400. Individual and married taxpayers earning over $75,000 and $150,000 respectively will get reduced payments with full phase-outs at $99,000 and $198,000. There are additional $500 payments for dependent children. For complete eligibility information please visit the IRS website.

- Will college students be eligible to receive a payment?

The CARES Act definition of eligible individuals excludes those who are claimed as a dependent on another taxpayer’s return. Accordingly, to the extent a college student is claimed as a dependent on the tax return of a parent, he or she would not be eligible for the rebate. For complete eligibility information please visit the IRS website.

- When will I receive my payment?

The Department of the Treasury intends to send the payments out as soon as possible. If you filed taxes in 2018 or 2019 and included your bank routing and account number for payments or refunds, and this information has not changed, the IRS has the information it needs to send your payment electronically. This could be as soon as the middle of April, according to Treasury. In addition, for Social Security recipients, the IRS will use direct deposit by the Social Security Administration to facilitate payments. If the direct deposit information you have provided in the past is for a bank-issued prepaid debit card, you will receive your funds on that card account. Recipients will be mailed a check if the IRS does not have your information on file. Check payments will follow weeks or possibly months after the direct deposits are sent.

- Can I receive my payment electronically if my current information is not on file with the IRS?

The IRS is developing an online portal so you can check the status of your information and your payment. That portal—which will be called “Get My Payment”—is expected to be available by April 17. In addition, the IRS has launched a new web tool allowing quick registration for those who don’t normally file a tax return. For the most up-to-date information, visit IRS.gov/coronavirus. While the IRS has extended the tax filing deadline this year from April 15 to July 15, another option is to file your 2019 taxes as soon as possible with bank routing and account number provided on the form.

- What if I am typically not required to file a tax return?

People who typically do not file a tax return and are not Social Security beneficiaries will need to file a simple tax return to receive an economic impact payment. Certain low-income taxpayers, veterans and individuals with disabilities who are otherwise not required to file a tax return will not owe tax. IRS.gov/coronavirus/economic-impact-payments provides information instructing people in these groups on how to file a 2019 tax return with simple but necessary information, including their filing status, number of dependents and direct deposit bank account information. As noted above, Social Security recipients who have not been required to file tax returns will not be required to file a tax return to receive their payments.

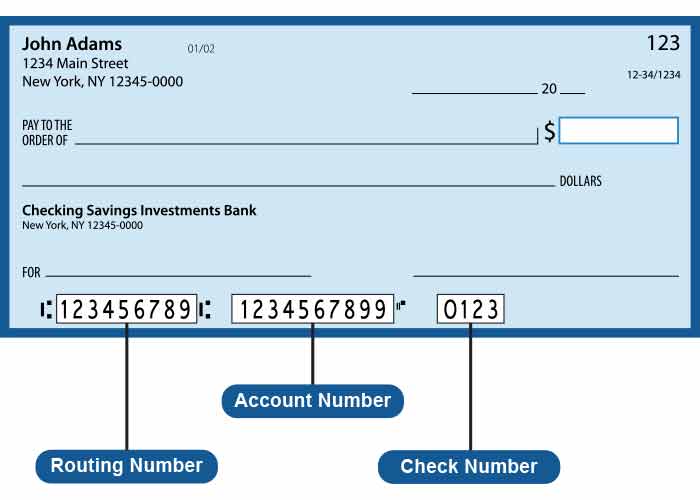

- What is a bank routing and account number?

Bank routing and account numbers direct payments to the right bank account at the right financial institution. If you have a checking account at a financial institution the information is on the paper check. The bank routing number is on the lower left-hand side of the check and tells Treasury the correct bank to send the payment. Your individual account number is to the right of the routing number. That tells the bank to credit your specific account. Bank-issued reloadable prepaid debit card accounts have the same numbers, but the way they are provided to you will vary.

- How do I find this information if I can’t find my checkbook or was never issued any checks at all?

Log in to your bank account online or by mobile app. Bank routing and account numbers may be located in different places in your app or online if you are logging in from a laptop or PC, depending on your bank. If you can’t find it easily, search “bank routing” within the app or website. If you still can’t find the information or can’t log on, call your bank for more information. You can also look up your bank’s routing number at aba.com/routingnumber. Please remember that to protect your finances from fraudsters, banks will not provide your account number over the phone.

Frontier Bank's Routing Number: 073921420

- I have a reloadable prepaid card with a bank. Can I direct the payment to that account?

Yes, follow the same instructions to gather the routing and bank account numbers to provide via the IRS online portal.

- I have a bank account. Can I still receive a paper check?

Yes, but be aware that your payment will be slower than an electronic transfer. Paper checks may be sent out weeks after the electronic checks are sent.

If you are willing to wait, we recommend that you deposit the check through remote deposit capture, if your bank offers this service. This is basically taking a picture of your check through your bank’s smartphone app. Follow the simple directions and you can make the deposit from the comfort and safety of your home the same day the check arrives in the mail.

Alternatively, you can make the deposit at your bank’s ATM.

The important thing to remember is that with branches closed or restricted, you may be required to visit a bank drive-through location if you want to deposit the check in person.

- I don’t have a bank account, but want to receive my money faster. What can I do?